First-Time Buyers using Help to Buy pay 10% more for new homes

First-Time Buyers in England buying a new home using the Government’s Help to Buy Equity Loan scheme are paying on average 10% more than those buying new homes without Help to Buy, reveals reallymoving in new research released today.

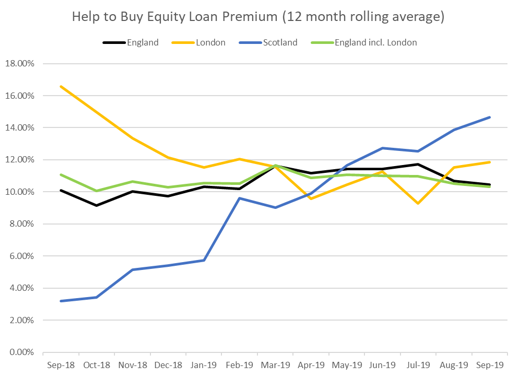

According to data collected from 41,500 First-Time Buyers using reallymoving for home move services over the last year, those purchasing a new build home with Help to Buy in England paid on average £303,450 in the twelve months to September 2019. Calculated at postcode area level to account for regional variations, the premium paid by those using Help to Buy Equity loans was 10.3%.

Graph 1: Help to Buy Equity Loan Premium – September 2018 to September 2019 (Source: reallymoving)

The Help to Buy scheme can seem like a lifeline for those struggling to raise a deposit, enabling them to buy a new home with just 5% equity, topped up with a Government loan of 20% (or 40% in London) which is interest-free for the first five years. However, this research indicates that the attractiveness of the scheme is enabling developers to charge more for homes with Help to Buy available and encouraging First-Time Buyers to pay over the odds. Last month housebuilding giant Barratt Developments announced pre-tax profits of £910 million, or £50,400 per home, with 40% of customers using Help to Buy Equity Loans.

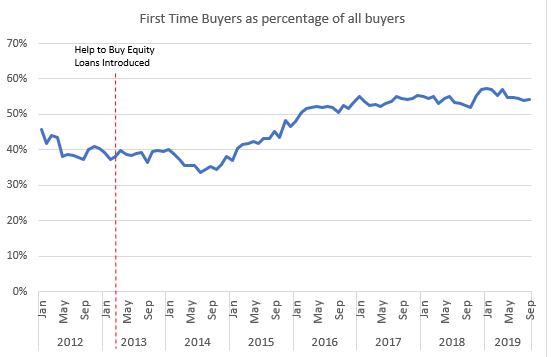

First-Time Buyers have been the backbone of the housing market over recent months accounting for 54% of all homebuyer activity in September 2019, down slightly from a peak of 57% earlier this year (see Graph 2). A competitive mortgage market and historically low interest rates have supported First-Time Buyer transactions, as well as the popularity of Help to Buy Equity Loans. The latest figures show that in September 2019 14% of all First-Time Buyers opted for a new build property.

Graph 2: First-Time Buyer activity as a proportion of all homebuyers (Source: reallymoving)

First-Time Buyers in north pay highest premium

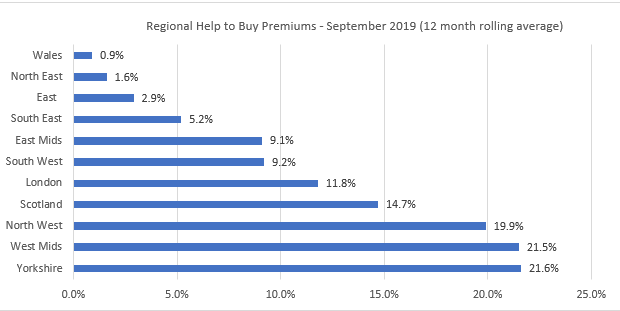

The Help to Buy premium is highest in the north and parts of the Midlands, with First-Time Buyers using the scheme in Yorkshire, the West Midlands and the North West paying approximately a fifth more (21.6%, 21.5% and 19.9% respectively) than those buying new homes independently (see Graph 3). Scotland has also seen a rapid increase in the premium paid by those using Help to Buy over the last year, peaking at 14.7% in September 2019.

In London, the Help to Buy premium has remained relatively stable throughout the past twelve months and currently stands at 11.8% – marginally higher than the England average.

Graph 3: Regional Help to Buy Equity Loan Premiums – September 2019 (Source: reallymoving)

The current Help to Buy Equity Loan Scheme will be replaced by a new version launching in April 2021 that will be restricted to First-Time Buyers only and for properties with a market value up to new regional price caps. It will run for two further years before closing in March 2023.

CEO Rob Houghton says:

“Help to Buy might be better named Help to Sell, since our research shows that despite the scheme’s popularity with buyers, housebuilders are the ones reaping the benefits. Most First-Time Buyers find it difficult to raise a deposit and as a consequence they are being cornered into the new build sector, where homes already command higher prices, before paying an additional premium on top if they need to use a Help to Buy Equity Loan. In many cases they simply don’t have the deposit required to explore other options such as buying a second-hand home, which may offer considerably better value.

“When buyers come to sell, they could find themselves in negative equity and unable to compete with new developments nearby offering Help to Buy, forcing them to accept a lower price. It’s important that those using the scheme consider their exit strategy, including whether or not they can afford the loan repayments on top of their mortgage when the interest free period comes to an end.”

Kindly shared by reallymoving.com

{kind=link}