First-time buyers continue to fuel the housing market, despite needing to buy a home

First-time buyers continue to fuel the housing market, despite needing an extra £7,350 income to buy a home, according to the latest Zoopla House Price Index.

Key points from publication:

- Annual house price growth slows to 3% with worst of the price falls over

- Demand continues to recover, with supply up 66% as the number of new sales rises above the five year average at Easter

- First-time buyers were largest buyer group in 2022 and expected to remain a strong source of sales in 2023, as steep rental market pushes FTBs into the market

- Income needed to buy a three-bed home for a first-time buyer has increased by an average of £7,350 since 2020 to a total of £55,900

- Three-bed homes remain the most in demand property for first-time buyers, but higher mortgage rates mean a clear shift toward two-bed homes

LONDON, 3 May 2023: The housing market continues to rebalance as buyer demand for homes reached its highest level so far this year, after Easter. Simultaneously, the stock of homes for sale continues to expand, boosting choice for homebuyers – now two thirds (66%) higher than this time last year.

Supply and demand rebalance generating new sales

Buyer demand for property remains 14% higher than 2019, but still 42% lower than levels seen this time last year, which was unusually high thanks to a chronic shortfall of homes available on the market. But with greater availability of houses to buy, prospective buyers now have more choice. As a result, this is having a tangible effect on new sales agreed, which are up 6% on 2019 and 10% ahead of the five year average after Easter.

Regionally, Scotland and the North East are seeing high levels of new sales agreed thanks to more attractive affordability levels. In London it’s a similar story, with a sustained period of weak price inflation over the last six years also helping to improve affordability.

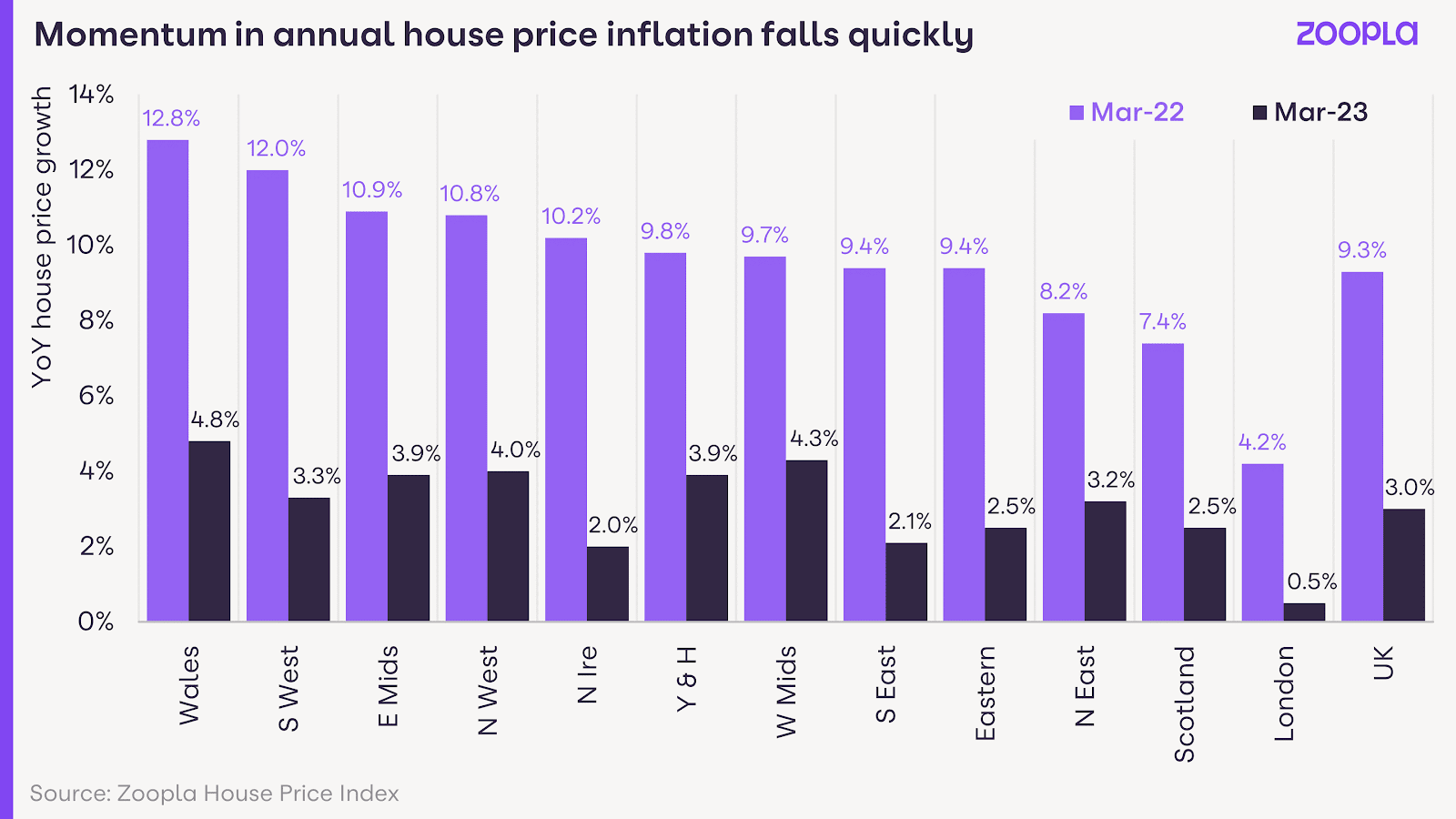

House price growth slows to 3% as worst of price falls over

The latest data from Zoopla reveals that UK house price growth has slowed to 3% as the market continues to register small quarter on quarter price reductions across the entire UK. Set against the lowest annual rate of house price growth since July 2020, house price growth varies from region to region with annual growth recorded at +4.8% in Wales and +0.5% in London – approximately less than a third of the levels recorded this time last year.

House price growth is also strong in areas that provide easy access to urban cities. For example, house price growth remains above average (over 5%) in areas such as Oldham in the North West, which is accessible to Manchester, Wolverhampton in the Midlands, near to Birmingham, and Selby in Yorkshire which is close to Leeds.

If current trends continue, UK house price growth is expected to reach -1% by the end of the year as the ongoing repricing of housing continues. Greater realism amongst sellers is supporting improving sales numbers – one in four homes (24%) available to buy in 2023 registered an asking price reduction, a level that is much lower than earlier this year and more evidence of a soft landing for house prices.

Steep rental increases pushing first-time buyers in to housing market

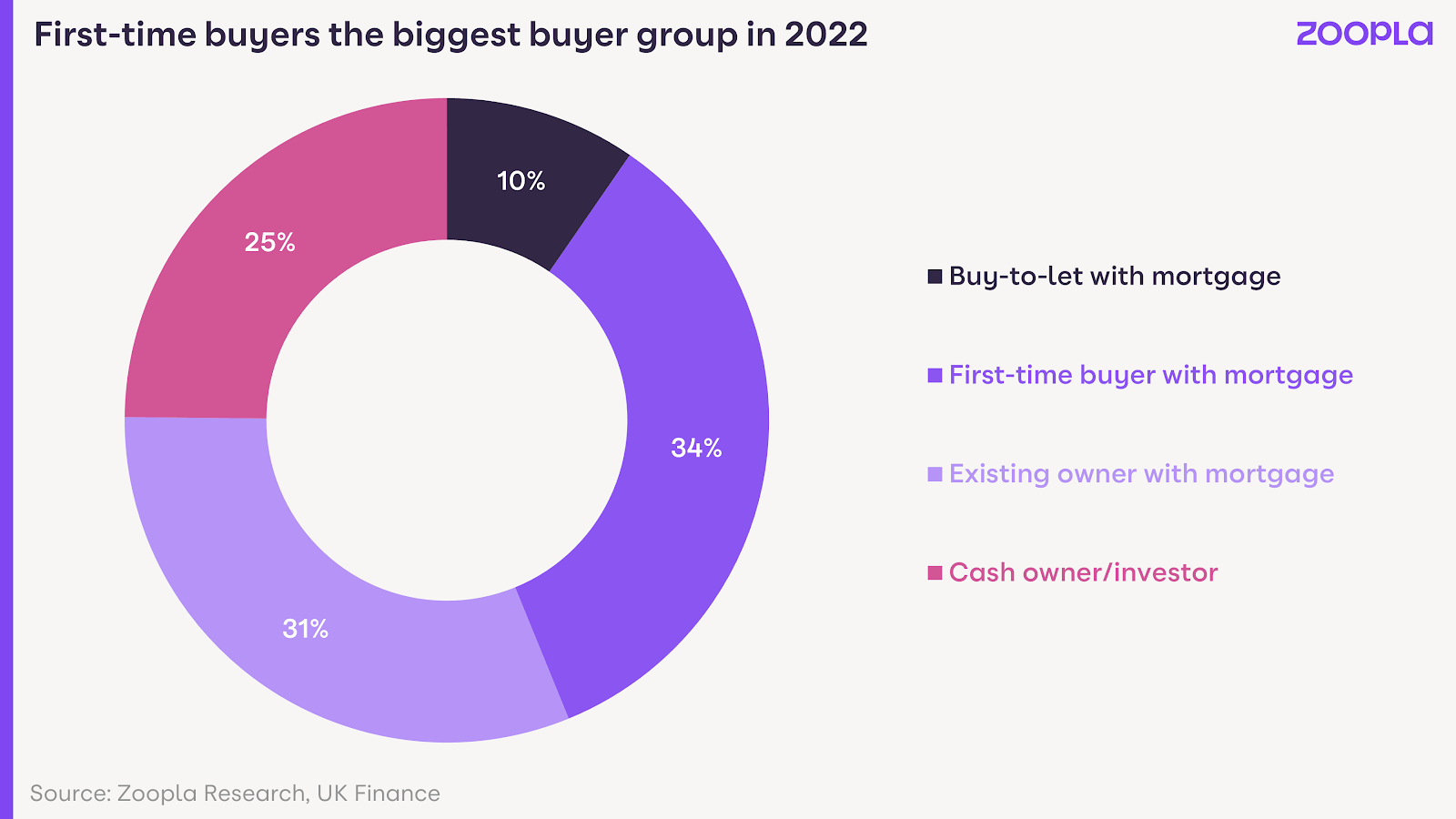

With deals to be done, first-time buyers (FTBs) continue to remain an important buyer group for the housing market as FTBs using a mortgage accounted for over one in three sales last year (34%). This made them the largest group of home-buyers after existing owners buying with a mortgage (31%) and cash buyers (25%).

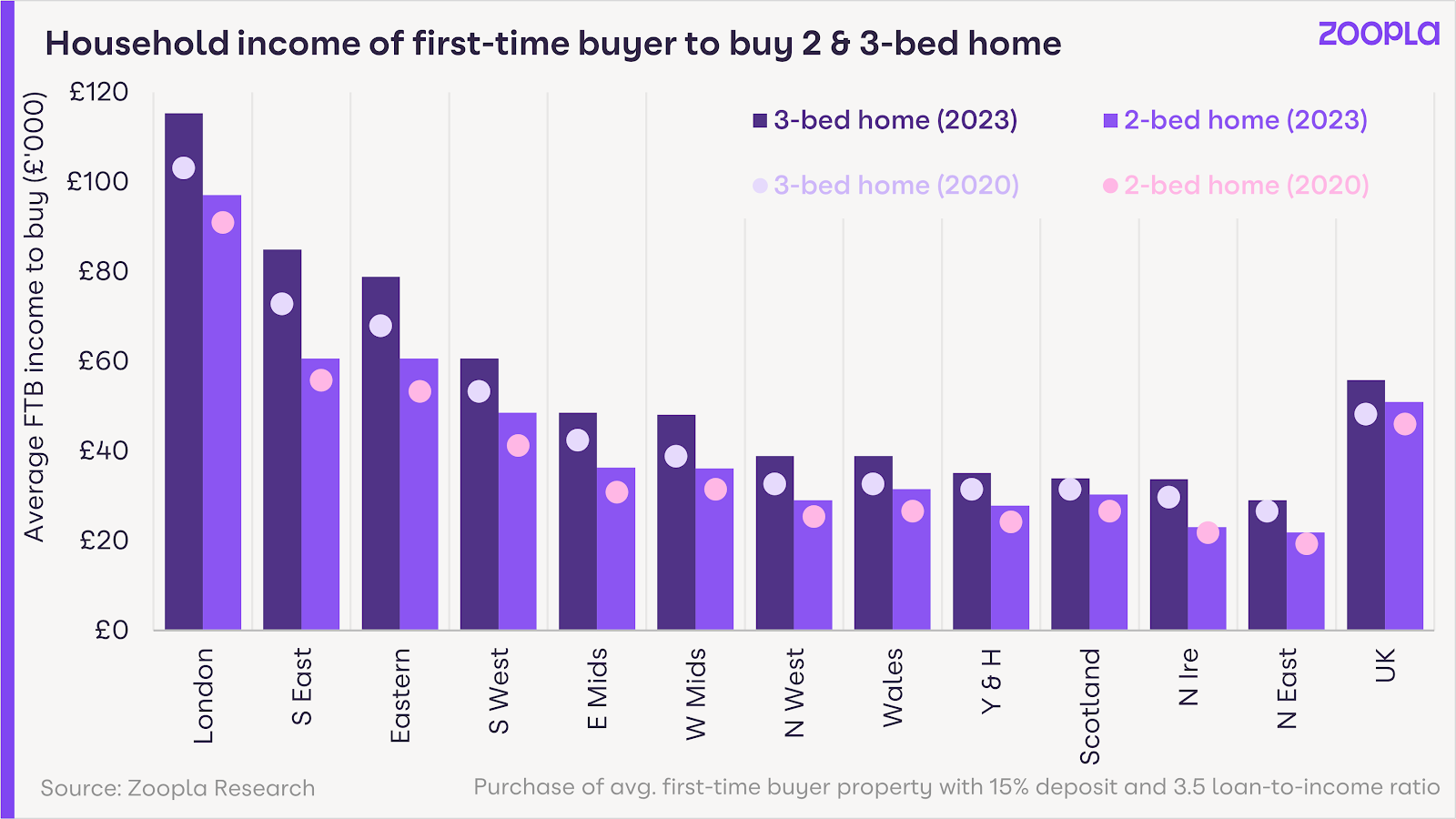

With rental costs up 11% or £1,120 over the last year, as well as a third fewer homes available to rent than the long run average, it’s no surprise that many are considering home ownership, provided they have the necessary deposit. However, FTBs now need an extra £7,350 on their gross household income to buy a three-bed house (a total of £55,900) versus an additional £4,900 required (a total of £51,000) to buy a two-bedroom home. According to ONS figures, the average income has only increased by £4,800 since early 2020.

Naturally, the income needed is even higher in areas such as London and the South East, where first-time buyers need an additional £12,150 on their gross household income for a three-bed property, or an additional £7,300 for a two-bed property.

Commenting on the latest report Richard Donnell, Executive Director at Zoopla, says:

“Housing market conditions continue to improve as buyers return to the market and more sales are agreed.

“House prices are posting very modest falls and are expected to be just 1% lower by the end of the year.

“The worst of the pricing adjustment appears to be behind us.

“We expect first time buyers to have another strong year in 2023 having been the largest buyer group last year.

“They need more income to buy but are starting to look for smaller homes and get away from rapid growth in rents.“

Mark Manning, Managing Director at Manning Stainton & Northern Estate Agencies Group, says:

“We have seen the market across our regions in the North of England show great resiliency with buyers still out looking in good number.

“The overall numbers of buyers searching may have fallen since a year ago but deeper analysis shows that when comparing with a more “normal market” such as that of 2018 or 2019 there is little change, particularly in first-time buyers who remain out in numbers searching for that first step on the ladder.

“Any decrease in buyers is largely due to the fall in the volume of investors and those looking to downsize.

“Clearly the increasing cost of finance affects those looking for the next buy to let and the lack of options for those looking to downsize remains a key concern but without government intervention it’s unlikely that this will change in the short term.

“We have seen prices fall back since the Summer of 2022 but those falls seem to have been isolated to the final quarter of that year with the price indexes catching up as those deals are now completing at the beginning of 2023.

“The average sale price on those offers agreed in 2023 indicate we will see very little change in the average price of property as we move into the summer and barring any significant further hikes in interest rates we expect prices to remain generally stable through the remainder of this year.”

Kindly shared by Zoopla

Main article photo courtesy of Pixabay

{kind=link}