Equity release market holds steady in the face of ongoing Covid lockdown measures

Equity release market holds steady in the face of ongoing Covid lockdown measures as identified in the Equity Release Council’s Q1 2021 market statistics.

1. Summary

Equity release market holds steady in the face of ongoing Covid lockdown measures:

- The first three months of 2021 saw £1.14bn released by 16,527 new or returning customers, a slight dip from £1.16bn from Q4 2020. Figures represent a 7% rise year-on-year from £1.06bn in Q1 2020 as market and consumer confidence proves more robust than in the first lockdown

- New customer activity in Q1 2021 cooled slightly, driven by seasonal trends amplified by renewed Covid-19 restrictions as the number of new plans edged down to 10,030 from 11,079 in Q1 2020

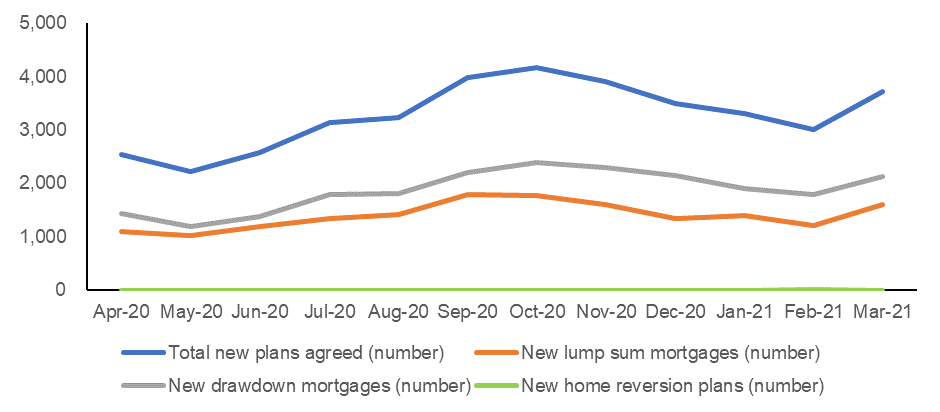

- With lockdown restrictions tightened, February 2021 saw the fewest new plans agreed since June 2020 before modest growth returned in March

- Figures come as the product choice for homeowners seeking to release equity reaches an all-time high, according to Moneyfacts¹

David Burrowes, Chairman of the Equity Release Council, comments:

“Despite ongoing uncertainty over the trajectory of the pandemic, this latest data for the early months of 2021 shows how the equity release market is following a steady course, albeit at a lower level than was the pre-Covid norm. The market has proven to be robust and applied lessons learned in the first lockdown to maintain access to property wealth for those customers who need it, guided by multi-layered financial and legal advice.

“Decisions to release equity are not made in isolation of wider developments in the property market. The resilience of house prices means that, for many older homeowners, property continues to be the most significant asset at their disposal and a viable route to boosting their income from pensions and savings, or gifting a ‘living inheritance’ to family members for their own use such as for a house deposit.”

“In the right circumstances, equity release is a flexible financial planning tool that can increase retirees’ options in later life. Property wealth has performed well even amid the economic disruption, and with the successful vaccination programme feeding through into consumer confidence, many people may be revisiting their financial priorities. It is vital to seek regulated financial advice and independent legal advice, ideally from Council members, to consider if equity release is right for you, or whether an alternative source of funds is more appropriate.”

2. Key statistics for Q1 2021

Overall activity:

- The total value of property wealth accessed by over-55 homeowners dipped slightly to £1.14bn in Q1 2021, from £1.16bn in the final quarter of 2020. However, the latest figure represents a 7% rise year-on-year from £1.06bn in Q1 2020.

- 16,527 new or returning customers were served during the first three months of 2021. This was down from 19,333 in Q4 2020, with normal seasonal trends accentuated by the return of strict lockdown restrictions.

- However, overall customer numbers proved more resilient than during the first lockdown of Q2 2020, when just 13,617 new or returning customers withdrew equity from their properties.

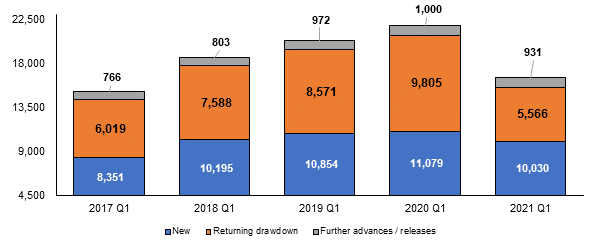

- Nevertheless, Q1 was the quietest start to a year for total customers served since Q2 2017, while the 5,566 returning drawdown customers was lower than at any point in the last four years.

Trends among new customers:

- 10,030 new plans were agreed in Q1 2021, down from 11,566 in Q4 2020. However, it should be noted the Q4 total was likely to have been heightened by delayed cases filtering through from earlier in 2020 after the lifting of the first lockdown.

- Product choices remained consistent with recent trends, as nearly three in five (58%) new customers opted for drawdown lifetime mortgages (vs. 57% in Q1 2020) and 42% opted for lump sum lifetime mortgages (vs. 43% in Q1 2020).

- February saw the fewest new plans agreed (3,003) since June 2020, with activity cooling for four successive months having reached 4,161 in October 2020. This is likely to be linked to the tightening of lockdown restrictions during this period, with activity beginning to recover again in March when 3,727 new plans were agreed.

- The average first instalment of a new drawdown lifetime mortgage reached £89,758, while the average new lump sum lifetime mortgage was £123,028. Member feedback suggests that increasing loan sizes can be attributed to a range of factors including:

- Customers taking advantage of having greater equity at their disposal as a result of rising property prices;

- Greater interest in releasing equity from wealthier customers with more valuable homes;

- Fewer customers using property wealth to fund smaller lifestyle purchases such as holidays during the pandemic, which reduces average loan sizes;

- More focus on repaying existing mortgage debt and gifting to family members to support their financial goals, including making their own house purchases while the current Stamp Duty holiday is available.

Trends among returning customers:

- Q1 2021 saw 5,566 existing customers with drawdown lifetime mortgages make use of their agreed reserves. This was down 18% quarter-on-quarter and 25% year-on-year as consumers acted conservatively rather than rushing to withdraw extra funds.

- 931 further advances were agreed between January and March enabling existing customers to access more property wealth. This was down from 1,000 in Q1 2020 and 975 in Q4 2020.

- Barring the low of 668 seen during the first lockdown in Q2 2020, the number of further advances agreed was the lowest quarterly figure recorded in two and a half years since Q3 2018 (902).

3. Market data

Graph 1: New equity release plans agreed per month, broken down by drawdown and lump sum lifetime mortgages – April 2020 to March 2021

Source: Equity Release Council

Graph 2: Equity release customers numbers during Q1 2017-2021, broken down by type of customer (new, returning drawdown and those seeking further advances)

Source: Equity Release Council

4. About the data

The Equity Release Council’s market statistics are compiled from member activity, including all national providers in the equity release market. This latest edition was produced in April 2021 using data from customer activity during the first quarter of the year (January to March). All figures quoted are aggregated for the whole market and do not represent the business of individual member firms.

Equity release products are available to homeowners aged 55+, enabling them to release money from the value of their home following a regulated process of financial advice and independent legal advice to determine whether this is suitable for their individual circumstances and long-term needs. Funds released are typically used for a range of purposes including providing additional retirement income, funding one-off expenses and lifestyle purchases, consolidating debts, meeting homecare costs and gifting a ‘living inheritance’ to family or friends.

For a comprehensive list of members, please visit the Council’s online member directory.

Sources:

¹ Moneyfacts: Choice for equity release seekers at all-time high, Monday 26 April 2021

Kindly shared by The Equity Release Council (ERC)

Main photo courtesy of Pixabay

{kind=link}