Equity Release Council: Q4 and FY 2020 equity release market statistics

The Equity Release Council have published their equity release market statistics for Quarter 4 of 2020 and for the full year.

1. Summary:

Pent-up demand and low pricing boost equity release market recovery in Q4

- Annual lending to new and existing customers totals £3.89bn as the equity release market shows resilience in the face of economic disruption

- A backlog of cases from earlier in 2020 contributed to a busy year-end as 11,566 new equity release plans were agreed by over-55 homeowners in Q4

- October saw the most cases completed as the market bounced back from the initial spring lockdown

- Caution remains as 2020 ends with 10% fewer new plans agreed than 2019, while 11% fewer customers sought further advances and 21% fewer made drawdowns from existing plans

- Favourable pricing saw the average equity release interest rate fall to 4.01% midway through Q4 2020, with the lowest rates at 2.30% [1] – less than the average 10 year fixed rate mortgage [2]

David Burrowes, Chairman of the Equity Release Council, comments:

“These figures offer encouraging signs of market resilience after a year that presented huge challenges to household finances and business operations.

“Over the last decade, releasing equity to boost your finances in later life has grown from a niche pursuit to a competitive market that has stabilised at £3.9bn of lending activity for the last three years, despite significant headwinds driven by Brexit uncertainty and the Covid-19 pandemic.

“The unusual patterns of activity in 2020 show some customers biding their time before accessing property wealth. New plans were delayed from earlier in the year and fewer customers have made use of drawdown reserves or sought extensions of existing loans. Releasing equity is not an overnight decision and should only be entered into after considering all alternatives.

“In the right circumstances, access to fixed lifetime products at lower rates than the average 10-year mortgage is a big factor in the appeal of modern-day equity release, as is the flexibility to pay interest or repay capital for many products to keep total costs in check. Ten years of transformation have made equity release an important financial planning tool that is increasingly valued by our ageing population.”

2. Key statistics for Q4 2020 and FY 2020:

Overall activity

- The final three months of 2020 saw 11,566 new plans agreed, making Q4 the busiest quarter of the year in line with normal seasonal trends despite being the quietest year-end since 2017.

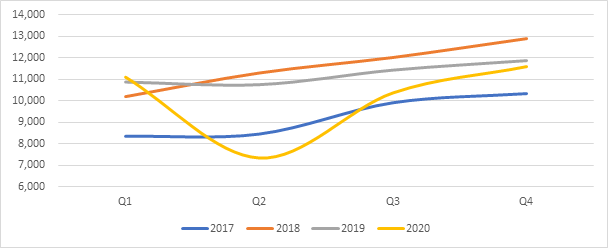

- 2020 saw 40,337 new plans agreed in total compared with 44,870 in 2019. Q4 activity was helped by pent-up demand from earlier in the year, as customers progressed plans that were put on hold when activity dipped to a four-year low in Q2 [see graph 1].

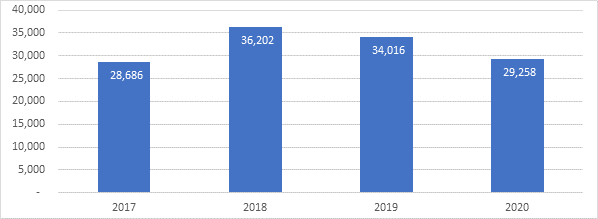

- During the nine months from April to December, new customer volumes have broadly reflected levels last seen in 2017 with 29,258 new plans agreed [see graph 2].

- The number of new and returning customers served in Q4 reached 19,333 to leave the annual total at 72,988. With new customer activity for 2020 down 10%, returning drawdown and further advance activity was the most subdued year-on-year (down 21% and 11% respectively).

- New and returning customers unlocked £1.16bn of property wealth in Q4, influenced by a moderate increase in average loan sizes and some customers accessing funds held back during lockdown when remote or desktop valuations temporarily replaced physical property surveys.

- Across 2020 as a whole, £3.89bn of property wealth was released by new and returning customers, down from £3.92bn in 2019 and £3.94bn in 2018. The disruption of the Covid-19 pandemic saw 57% of lending activity concentrated in the first and final quarters of 2020.

Trends among new customers

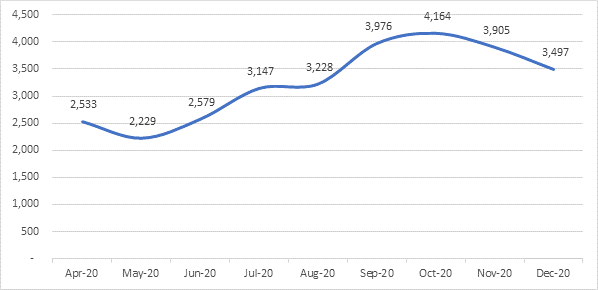

- October saw the most new plans agreed in Q4 (4,164) as the UK experienced a respite from lockdown conditions. This continued the recovery that developed from May to September before activity then slowed during the final two months of the year [see graph 3].

- Almost three in five new customers (59%) opted for drawdown lifetime mortgages in Q4, down slightly from 61% a year earlier.

- Lump sum lifetime mortgages made up 43% of new plans agreed across the whole of 2020. This is the largest annual share of activity since 2009 (44%) and likely to be influenced by customers with interest-only mortgages reaching maturity.

- The average new lump sum lifetime mortgage agreed in Q4 was £104,501, an increase of 3% from Q4 2019 (£101,058).

- Over the course of 2020, new customers taking out drawdown lifetime mortgages have increased their total plan size by 7%, with an average of £81,724 taken up front in Q4 as a first instalment and £33,511 held in reserve for future use.

Trends among returning customers

- Q4 2020 saw 6,792 existing customers with drawdown lifetime mortgages make use of their agreed reserves. This was broadly consistent (up 1%) from 6,697 in Q3 but remained 25% down from 9,096 in Q4 2019.

- The average instalment taken by returning drawdown customers of £11,520 was also consistent with the previous quarter (£11,424) and 11% lower than in Q2 (£13,005) when the first national lockdown was in place.

- Further advance activity also remained subdued in Q4, with 975 extensions agreed to existing equity release plans. This compares to 1,106 in Q3 2020 and 1,141 in Q4 2019.

3. Market data:

Graph 1: New equity release plans agreed per quarter, 2017 to 2020

Graph 2: New equity release plans agreed between Q2 and Q4, 2017 to 2020

Graph 3: New equity release plans agreed per month, April 2020 to December 2020

[1] Source: Moneyfacts data for November 2020

[2] Source: Bank of England data for November 2020 shows the average 10-year fixed mortgage rate at 75% loan-to-value (LTV) was 2.55%.

Kindly shared by Equity Release Council

Main article photo courtesy of Pixabay

{kind=link}