Buy-to-let mortgage lenders are largest for 2018, according to UK Finance

For the first time, we are today publishing data showing ranking tables of buy-to-let mortgage lending in 2018 by UK Finance mortgage members.

Earlier this year, we published the value of all outstanding and new residential mortgages for individual borrowers only, consistent with mortgage lending data published by the Bank of England.

The different customer base covered by these buy-to-let data, includes loans for both individuals and companies, thus reflecting the full sweep of lending to landlords for residential property, regardless of how they are structured. Commercial buy-to-let mortgage loans, such as properties rented out for office space, are not included.

As our largest lender tables for full market and buy-to-let mortgage lending are based on these different bases, it is not possible to infer any one lender’s residential mortgage business by subtracting one from the other.

In 2018, gross buy-to-let mortgage lending totalled £40.5 billion, up 5.5 per cent on 2017. Competition in the sector is strong, despite tax changes for landlords and regulatory interventions over the past few years, so that we see 53 lenders covered by our table for gross lending.

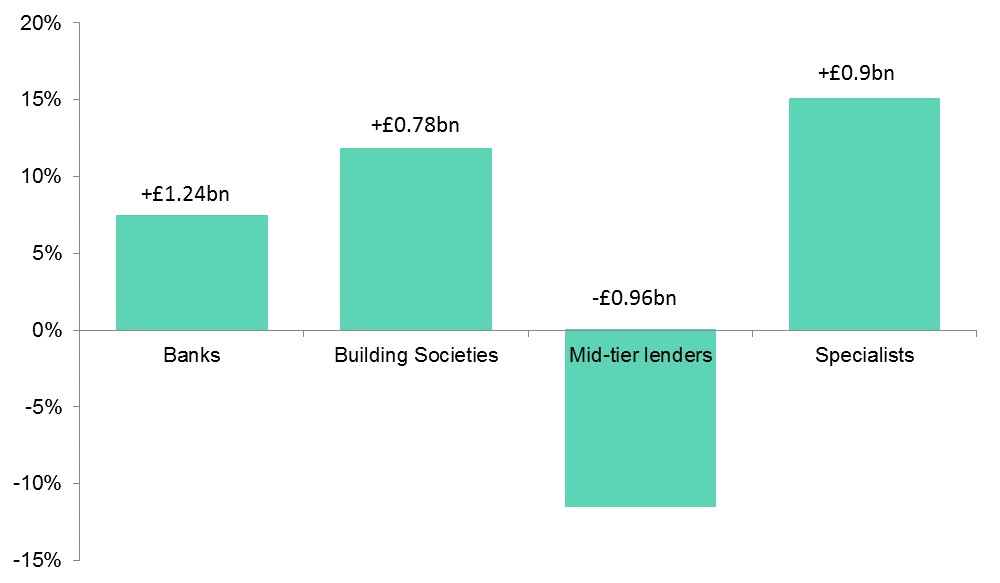

Chart 1: Growth in gross buy-to-let lending by lender type, 2017-2018

Source: UK Finance Largest Lenders

Specialist lenders and building societies (many of whom conduct buy-to-let activity within specialist lending subsidiaries) saw the strongest percentage growth, helped in part by their more tailored approaches to underwriting. Manual underwriting has allowed these lenders to cater for applications which do not easily fit through the (necessarily) more automated underwriting processes of many larger lenders.

These lenders are also able to adapt their underwriting quickly to the changing demands of the market and the regulatory requirements surrounding it, for example lending to limited companies, and to portfolio landlords (those with four or more properties).

With more and more lenders competing within the buy-to-let space, we have seen products become more affordable for landlords, even within the more complex cases where tailored underwriting is required.

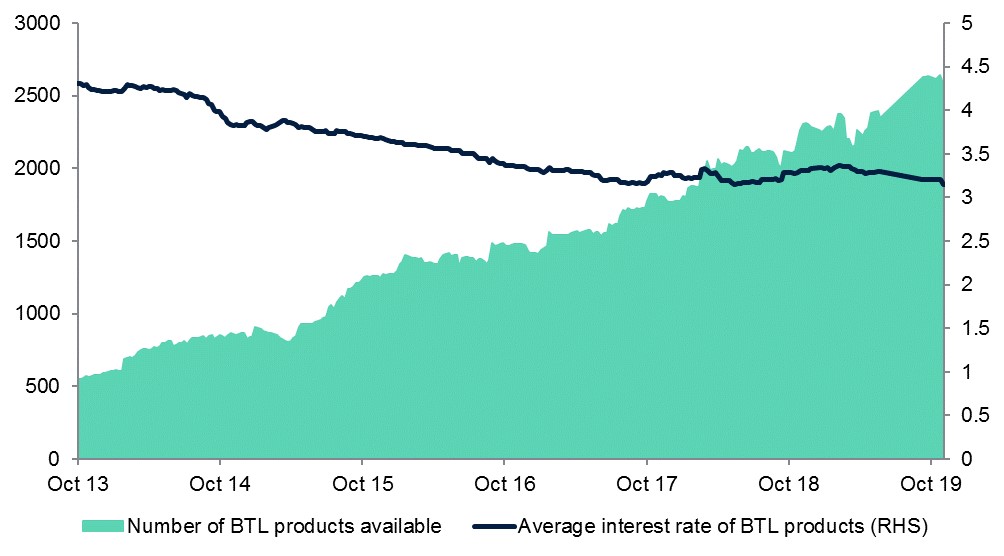

Chart 2: Volume and average interest rate of available buy-to-let products, 2013-2019

Source: Moneyfacts

Our figures show that, despite challenging conditions in the buy-to-let market, lenders are continuing to support and work with landlords, to ensure sustainable and affordable finance is available for the private rented sector.

Kindly shared by UK Finance

{kind=link}