Over Half of Older Homeowners Factor Property into Their Financial Plans as Attitudes Shift in Later Life

Equity Release Council report – Beyond bricks and mortar: the changing role of property in later life financial plans – supported by Key.

- As national property wealth passes £4 trillion, older households depend the most on this source of finance: making up 40p in every £1 of over-65s’ wealth and 47p among over-75s

- 51% of homeowners aged 45+ see money invested in property as part of their later life financial plans, with those aged 45-64 most likely to agree

- 44% feel taking out a mortgage or loan to access property wealth in later life is becoming a more common way to manage money, while 40% see it as a “reality” of ageing

- Retirees of tomorrow increasingly plan to use money invested in property to help family members while they are still alive or as a ‘nest egg’ for unexpected expenses

- Report calls for action to meet later life and intergenerational needs – including a Later Life Commission and Minister for the Elderly alongside industry and regulatory efforts

More than half (51%) of homeowners aged 45 and over see money invested in property as part of their financial plans for later life, according to a new report from the Equity Release Council.

“Beyond bricks and mortar: the changing role of property in later life financial plans”– supported by Key, the UK’s leading independent equity release adviser – examines trends in UK property wealth and how it is impacting homeowners’ outlook in later life both in terms of managing their own finances and supporting younger generations.

It shows older homeowners – particularly those aged 45 to 64, the retirees of tomorrow – are reassessing the traditional roles of property in retirement funding and inheritance.

A picture of UK property wealth

The Council’s analysis shows net property wealth has passed £4 trillion – the equivalent to nearly £80,000 for every UK adult, with investment in property exceeding new mortgage debt every year since 2008. Three quarters of the average home is now owned outright, and regular mortgage capital repayments alone have steadily increased from £30bn in 2007 to £50bn in 2018.

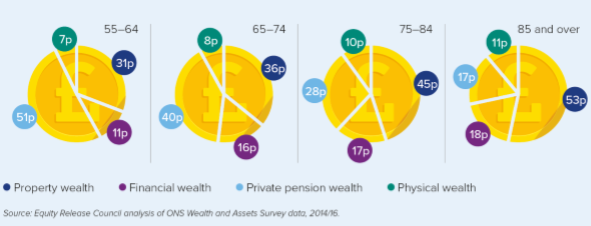

Older age groups are not just the biggest owners of property; they also depend the most on its contribution to their overall finances. Bricks and mortar accounts for 40p in every £1 of household wealth for those aged 65+, rising to 47p among the over-75s versus 35p across the nation.

Graph 1: The changing makeup of household finance in later life

Shifting perceptions of property

The report suggests these shifting trends are driving a change in attitude among the over-45 homeowner population. Many are facing multiple financial challenges as they seek to live longer, healthier lives while balancing their needs with providing support for younger generations.

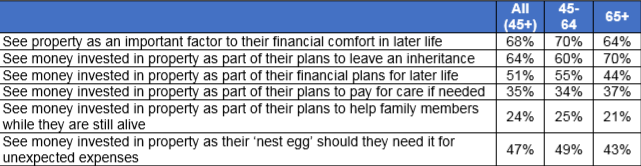

Homeowners aged 45+ see property as the most important contributing factor to their financial comfort in later life (68%), and over half (56%) feel they can benefit from its financial value while they still live there.

The retirees of tomorrow – those aged 45-64 – are less likely than their older counterparts to see property as something to leave behind as an inheritance. Instead, they are more likely to think of it as a multi-purpose financial tool that can support their own financial plans (55%), be used as a nest egg to meet unexpected expenses (49%) or help family members (25%).

Table 1: Attitudes to the role of property in later life among homeowners aged 45+

Re-evaluating later life lending

More than two fifths (44%) of over-45 homeowners feel taking out a mortgage or loan to access property wealth in later life is becoming a more common way to manage money, while 40% see it as a “reality” of ageing. Only 34% feel they have no need to consider this option either now or in future, including just 30% of those aged 45-64.

While there is significant intent to use – or at the very least consider – residential property as part of later life planning, current activity suggests more needs to be done to encourage people to take proactive steps.

To address this, the Council has called for action spanning consumers and their families, industry, regulators and government, to support financial education, product development, consumer safeguards and policy planning. This includes establishing a cross-party Later Life Commission and a dedicated Minister for the Elderly (see notes to editors for more details).

David Burrowes, Chairman of the Equity Release Council commented:

“The UK’s ageing population and changing retirement landscape means people are increasingly thinking of property as a multi-purpose financial asset – particularly those aged 45 to 64, the retirees of tomorrow. Property is often a person’s single largest asset and makes a significant contribution to homeowners’ personal finances as well as providing a place to live.

“Changing attitudes to property are significant given the financial challenges facing our ageing population as they seek to live longer, healthier lives. Many people have made inadequate provision for their retirement and care needs, while others have younger family to support. Consequently, bricks and mortar have become a vital piece of the retirement funding jigsaw, to benefit people during their lifetime as well as their families.

“Our calls to action are underpinned by the core belief that – while drawing on property is not right for every circumstance and should not distract from encouraging long-term saving – it should be on every homeowner’s checklist to consider in later life, now more than ever. We urge industry and policymakers to evolve their thinking to reflect that of older homeowners to support this emerging demand.”

Will Hale, CEO of Key – the UK’s largest independent equity release adviser – commented:

“For over-65s today, wealth is intrinsically linked to bricks and mortar with 40p in every pound that they own tied up in property. Historically, people have seen their house as a home and potentially as an inheritance to pass on to the next generation but this report clearly highlights that not only is that perception changing but, given the increasing pressures on retirement finances, that it has to change.

“With pension savings failing to keep up with the increase in longevity, the vast majority of people will need to carefully consider how they maximise all their assets in retirement. Whether they conclude they want to use property wealth to fund one-off purchases in later life, a source by which to top-up regular income or to provide a helping hand to the younger generation, ignoring 40% of their net worth just doesn’t make sense.

“This report and its recommendations clearly highlight not only the potential benefits that housing equity can bring to older homeowners, their families and the nation as a whole but the size of the challenge that we are facing.”

Kindly shared by Equity Release Council

{kind=link}