HomeTrack publish their UK House Price Index for June 2022

HomeTrack publish their UK House Price Index for June 2022, which shows house prices continuing to grow with house price inflation at 5% for the year.

Key points from publication:

- Market activity resilient in the face of economic headwinds

- One-off pandemic impacts have continued to support the desire to move, and sales volumes in H1 which are 10% down on last year.

- Total sales set to exceed our original projections – we expect 1.3m sales completions in 2022, 100,000 higher than forecast.

- More activity means the rate of price growth will not slow as fast as we expected, even if there were sharp drop in demand.

- We expect house prices to end the year 5% higher over 2022.

- The market is not immune from higher borrowing costs. Levels of activity will slow faster over Q3 and into Q4. The scale of the slowdown will depend upon how high mortgage rates rise.

|

+8.3% Current UK house price growth |

1.3m Projected sales volumes in 2022 |

+5% Projected house price inflation by end 2022 |

Market activity resilient and set to out-perform in 2022

House price growth and sales volumes are proving more resilient than many might have expected given the increases in the cost of living and initial increase in mortgage rates. The housing market is not immune to these growing economic headwinds but there are good reasons why market activity has been holding up.

We expect demand for homes to weaken later in the year, but we are revising up our forecasts for house price growth and sales volumes for 2022.

House price growth starting to slow off a high base

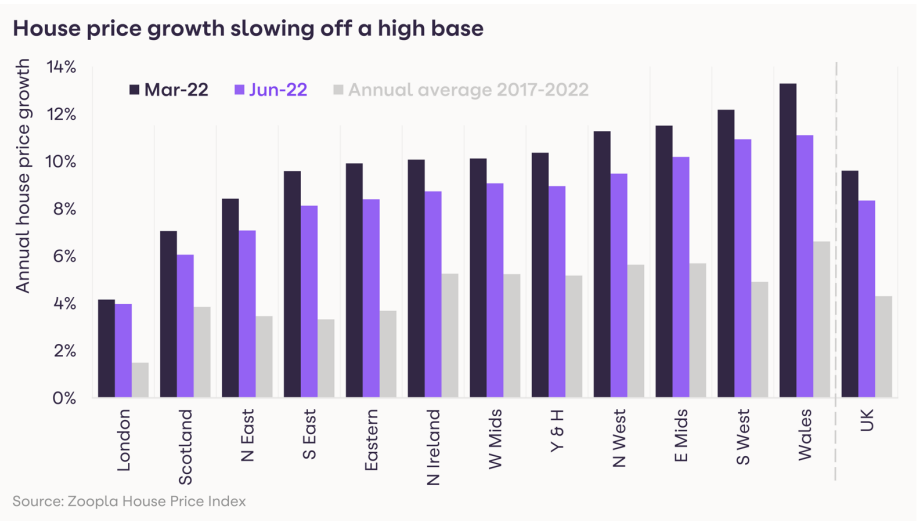

Average house prices are up 8.3% over the last 12 months, lower than the recent high of 9.6% in March 2022. Around the country, prices are rising fastest in Wales (+11.1%) and remain in double digits in the South West and East Midlands. London continues to lag well behind with average prices up 4% over the last year.

All markets are registering slower growth off a high base. The rate of price increases remains well ahead of the 5-year average – see chart below. We expect the rate of growth to slow over the second half of the year, but not as fast as we had projected at the end of last year due to the continued resilience in sales and buyer interest.

Pandemic impacts continue to stimulate home moves

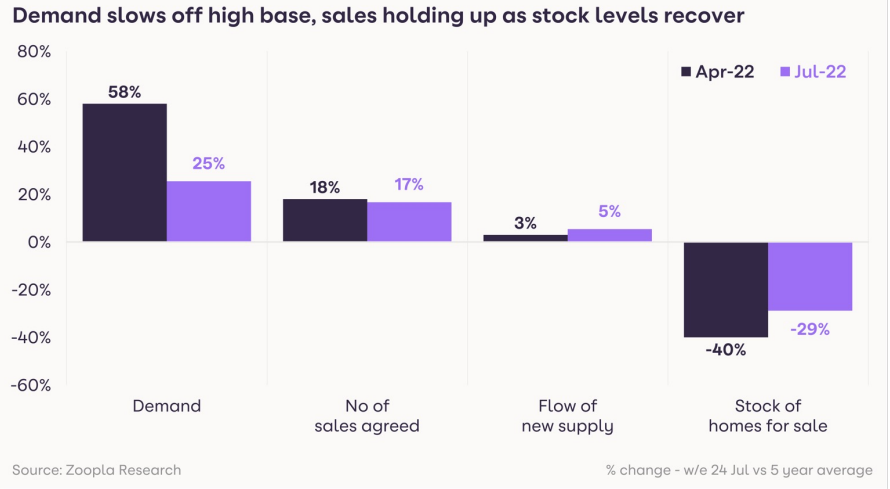

Our latest data shows demand for homes remains 25% above the average over the last 5 years. Buyer interest has slowed over recent months from high levels registered in the Spring, but levels of demand remain on a par with this time last year. The headwinds facing consumers will be starting to squeeze some people out of the market, but this is being offset by those with a continued desire to move. There are several factors at play, largely pandemic-related.

Link between working from home and desire to move

Pandemic factors continue to influence housing market activity and greater flexibility in the labour market is stimulating more home moves. A recent consumer survey by Zoopla found a strong link between increased expectations of working from home and the scale of the eagerness to move in the next 12 months. Those who expect to work at home more are 5x as likely to move than those that expect no changes in working patterns.

Around a third of the workforce has the ability to work more flexibly. Furthermore, a recent report1 from the Office for National Statistics found that levels of homeworking have more than doubled over the pandemic with an additional 5m homeworkers, taking the total to 9.7m. Only a small proportion of these homeworkers needs to move in order to support overall sales volumes.

In addition, these changes may support first time buyers who, rather than waiting to save up a bigger deposit in order to live close to work in a higher value area, could potentially buy sooner by purchasing further afield in an area offering better value for money.

Older workers leaving the labour market

Another impact of the pandemic has been over half a million older workers (50-70 year olds) leaving the labour market over and becoming economically inactive (ONS2). Retirement is the biggest driver and one important life-stage trigger for home moving decisions. Older owners with excess space who are retiring or otherwise may be additionally motivated to move by concerns over the cost of living and running costs of their current home. This could apply to other types of households as well.

Sales volumes expected to be 8% higher than expected

These pandemic factors explain why sales and price growth has remained more resilient than we might otherwise expect given the economic headlines. If we didn’t have them then the market would be slowing far more quickly than it is currently.

The net result of these trends is that we expect housing sales to outperform our original forecasts for 2022. Year to date sales agreed are only 10% lower than this time last year, even allowing for a slower H2 we expect overall housing sales to total 1.3m. This is 100,000 (8%) higher than the 1.2m we projected at the start of the year.

Resilience of buyer demand more varied at a local level

While at a headline level the demand for homes is on a par with this time last year and 25% above the 5 year average, there are local markets where demand is weaker than the national picture and those where buyer interest remains stronger. As a ‘point in time’ view, the chart below plots the strongest and weakest postal areas for buyer demand in the last month compared to the 5 year average.

We find that demand for homes is has been weakening in some of the areas registering high rates of price growth in the last 2 years, particularly in the South West of England and parts of Wales and the areas bordering England. In addition, buyer interest remains weak in the most unaffordable markets, primarily parts of London where the impacts of the pandemic have shifted the profile of housing demand and price growth remains well below average.

In contrast, there are markets where sales demand remains strong and well above average, despite increases in the costs of living and mortgages. These are typically more affordable cities or markets well connected to large cities, or a combination of the two. These areas are all registering above average levels of house price growth driven by enabled by more attractive affordability levels.

Affordability dictates the pace and scale of price rises

This analysis demonstrates that while the direction of house price growth is dictated by the balance of demand and available supply, the pace of price changes is dictated by housing affordability. The Zoopla house price index shows that the fastest price gains continue to be seen in the most affordable housing markets while unaffordable markets lag behind as affordability pressures price out growing numbers of households and limit the potential for price gains. There is still scope for prices to rise further in some markets.

Trajectory of borrowing costs core to housing outlook

We expect house price growth to continue to slow over the remainder of 2022 but at a slower rate than we originally expected. With average house prices already having grown 3.6% over the first half of the year, we expect them to increase further ending the year 5% higher over 2022 as a whole.

The pandemic factors stimulating demand will continue to play a role but the outlook for housing demand really hinges on how high interest rates rise in order to bring inflationary pressures under control. Interest rates are a blunt tool that hit demand and economic growth.

Mortgage rates have already jumped to around 3.5% from recent lows of sub 2% – see chart. They look set to move higher, towards 4% over the rest of the year taking them back to 2013-2015 levels.

Our analysis suggests 4% is a key level for mortgage rates and one beyond which we would expect to see zero annual house price growth. Were rates to go even higher then modest price falls are a likely consequence as demand is squeezed and we see more of a buyers’ market.

The positive news is that the housing market is in a much better market is in a much better position to weather a sizable jump in mortgage rates than has been the case in previous economic cycles. This because housing is not materially over-valued or reliant on borrowers using high levels of leverage or stretching incomes to bid up prices as we have seen in the run up to previous downturns. This is largely thanks to mortgage regulations introduced after the global financial crisis.

Talk of major price falls seems wide of the mark but the shift from a prolonged period of cheap money to one of higher borrowing costs will have greater influence on the housing market into 2023.

Richard Donnell, Research Director, said:

“A lack of any major over-valuation of UK housing – thanks to mortgage regulation – means the market is in much better shape to weather the economic challenges ahead than in previous economic cycles, but it’s not immune.”

Kindly shared by Hometrack

Main photo courtesy of Pixabay

{kind=link}