Home-sellers give up third of recent price gains to achieve a sale

Home-sellers give up third of recent price gains to achieve a sale – discounting on average £14,100 – according to the Zoopla House Price Index, published today (28 February 2023).

Key points from publication:

-

- Annual house price inflation slows to 5.3% – down from 8.6% last year

- Buyer demand and sales volumes are 20-50% lower than a year ago, but slightly ahead of the pre-pandemic years (2017-2019)

- Sellers are having to accept an average 4.5% discount to the asking price to achieve a sale – highest for five years as buyers’ market takes hold

- Average discount to asking price is £14,100, meaning sellers are having to forgo a third of their pandemic house price gains

- The average UK home grew in value by £42,000 over the pandemic, suggesting sellers are forgoing, on average, 33% of their pandemic gains

- UK house price inflation set to move into low negative year-on-year by summer; however, it’s still on track for a ‘soft landing’ with modest price falls of up to 5% and 1m sales in 2023

The latest House Price Index from Zoopla – the leading property website – reveals sellers are having to discount their home by an average of 4.5% to achieve a sale as the shift to buyers’ market continues.

Asking to achieved price gap widens to largest for 5 years as buyers’ market takes hold

The asking-to-achieved price gap has widened to its largest for five years. While sales volumes have recovered, the average discount to achieve a sale has increased over the last five months and currently stands at 4.5% – an average £14,100 discount per sale. For context, the average UK home grew in value by £42,000 over the pandemic, suggesting sellers are forgoing, on average, 33% of their pandemic gains.

Whilst negotiating down from the asking price was normal practice before the pandemic boom in England, Wales and Northern Ireland, in Scotland, most homes remain marketed as ‘offers over’. Discounts to asking price are larger than in the pre-pandemic years and reflect the rapid transition from a hot sellers’ market – where most buyers had to pay the asking price over much of 2021 and 2022 – to a buyers’ market. This transition to a buyers’ market is accompanied by nationwide repricing as the market adjusts to the reduction in buying power thanks to higher mortgage rates impacting buyer affordability.

Buying power is starting to recover as mortgage rates fall from their 6% highs of late 2022, however even at 4%, the average home buyer has a fifth (20%) less buying power than they did a year ago when mortgage rates were 2%.

Supply returns to ‘normal’ levels, boosting buyer choice

Demand from home buyers has rebounded in the first two months of 2023, but remains at half the level recorded a year ago as buyers remain cautious. Volumes of sales agreed in early 2023 have recovered, tracking the usual seasonal upturn seen post-Christmas, albeit a quarter (24%) lower than this time last year.

In contrast to 2022, stock of homes for sale is up by over 60% compared to last year, with market supply returning to normal. The reality is that current market conditions are more aligned with pre-pandemic years, with demand 8% higher and sales agreed up 1% – in the four weeks to the 19 February 2023 compared to the same period between 2017 and 2019.

The average estate agent office has 24 homes for sale compared to just 15 a year ago, creating more choice for home buyers who now have more room to negotiate on price and in turn, helping to reduce the upward pressure on house prices.

Sellers – supported by agents – are adjusting asking prices in the face of weaker demand with over 40% of homes currently listed for sale on Zoopla having had their asking prices reduced to attract price-sensitive buyers.

Looking ahead, small month-on-month price reductions are expected over the next 2-4 months as a soft reset in house prices continues. By the summer, modest annual price reductions of up to 2 or 3% are anticipated.

Activity levels holding up in more affordable markets

While overall sales are lower year-on-year, they are ahead of the pre-pandemic years in more affordable housing markets such as the North East and Scotland due to higher mortgage rates having less of an impact on demand in lower-value markets. In contrast, sales in the Midlands and southern England are up to 9% lower compared to the pre-pandemic period.

Higher house prices in these regions have a greater impact on buying power and the level of demand from would-be buyers. In London, sales are 4% above their pre-2020 levels and although the capital is far from affordable, its housing market has significantly underperformed compared with the rest of the country since 2016. This gives the appearance of offering more value for money which is supporting sales.

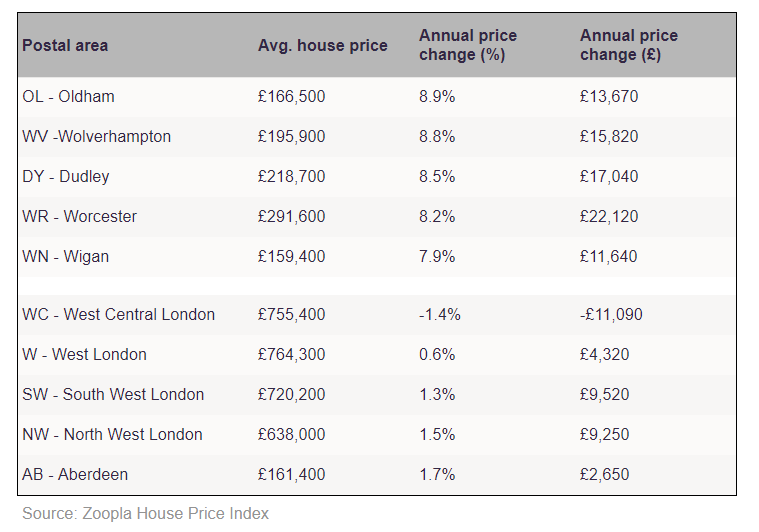

Within the UK, annual house price growth rate ranges from +2.5% in London to +7.1% in Wales. The real weakness in price inflation is in southern England where high house prices compound the impact of higher mortgage rates on buyers. Above average house price growth continues in affordable regional towns near larger urban centres such as Oldham, Dudley, Wolverhampton and Worcester where price inflation remains over 8%. Inner London areas continue to top the list with the weakest rates of annual price growth although no postal areas are registering year-on-year price falls at this stage.

Top 5 and lowest 5 areas by annual price changes in the UK by postal area:

Richard Donnell, Executive Director at Zoopla, says:

“Greater realism on the part of sellers is supporting housing market activity in the face of higher borrowing costs.

“Many homeowners are sitting on sizable house price gains made over recent years and have more room to be flexible accepting offers below the asking price.

“Discounts to asking price have widened and while 4-5% discounts are manageable, if these were to widen further then this would point to a greater likelihood of larger house price falls.

“We believe the market remains on track for a soft landing in 2023 with modest price falls of up to 5% and one million housing sales.”

Matthew Thompson, Head of Sales at Chestertons, says:

“London is very much an isolated market in a sense that demand and supply levels are different to the national picture.

“The capital tends to experience a chronic undersupply as demand for properties is ongoing.

“As such, 2023 started off with high demand from buyers booking in viewings and wanting to finalise their move as soon as possible.

“Sellers, on the other hand, have remained hesitant about putting their property up for sale amid economic uncertainty.

“As we are approaching Spring, which is known as the busiest period for the property market, and the Bank of England shared a more positive view on the economy, we are expecting more sellers to enter the market.

“This increase in properties being put up for sale will inevitably lead to a more balanced market environment and allow buyers to negotiate the asking price to a certain degree.”

Kindly shared by Zoopla

Main article photo courtesy of Pixabay

{kind=link}