Equity Release Council: Q2 2020 equity release market statistics

The Equity Release Council has published its Q2 2020 equity release market statistics, showing initial recovery signs in June after Q2 activity fell.

Headline summary:

- £698m of property wealth was accessed by older homeowners in Q2 2020, down by 34% – almost £400m – from the previous quarter.

- The fall reflected wider lending trends – Bank of England data for April and May shows gross lending secured on dwellings was down 36% from February and March*.

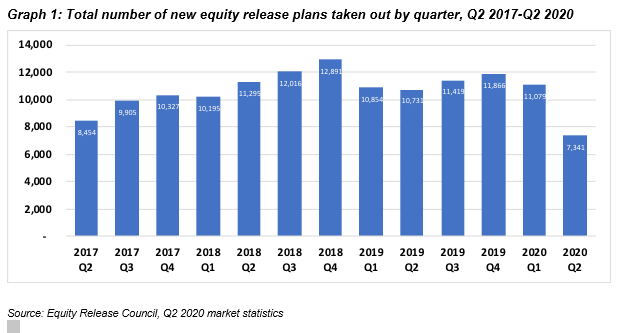

- The number of new equity release plans agreed between April and June also declined by 34% from 11,079 in Q1 2020 to 7,341.

- May was the quietest month for new plans before initial signs of recovery followed in June as lockdown conditions began to ease.

- Customers held back from making further drawdowns from existing plans or seeking further advances as they waited to see the long-term impact of Covid-19.

David Burrowes, Chairman of the Equity Release Council, comments:

“Equity release market activity continued to mirror wider economic conditions, with the confidence of early 2020 giving way to caution as households assess the impact of coronavirus on everyday life.

“Careful precautions have kept the market open to those who wish to choose the option of equity release and ensured customers have access to property wealth to help meet important financial and social needs. That said, the fall in the number of new plans and fewer returning customers accessing extra funds are clear signs of people pausing to see how the wider situation unfolds.

“Property assets have long been one of the nation’s main sources of wealth and are likely to play an increasingly important role to support people when addressing the challenges facing many in later life, including bridging the savings gap for older homeowners who are asset rich but cash poor. Releasing equity is not a suitable choice for everyone, and our focus is on ensuring customers’ interests are protected at every stage of the process through structured financial advice, independent legal advice and clear product safeguards.”

Key statistics for Q2 2020:

Overall activity

- The 7,341 new equity release plans taken out between April and June was the lowest seen in any quarter in the last four years since Q2 2016 (6,671), down from 11,079 in Q1 2020.

- The total number of customers (new and returning) served in Q2 2020 was 13,617, down from 21,884 in Q1 2020 (-38%) and 20,866 in Q2 2019 (-35%).

- £698m of property wealth was accessed by new and returning customers, a reduction of almost £400m from £1.064bn in Q1 2020.

Monthly trends

- May was the quietest month for new plans agreed, with just 2,229 completions compared to an average of 3,693 per month during Q1 2020 (a 40% drop).

- April’s total of 2,533 new plans completed was likely to result from cases arranged earlier in the year, before the nationwide lockdown came into effect in late March.

- With England’s housing market reopening in mid-May, the number of new plans completed recovered slightly in June to 2,579, but remained 30% down on the average monthly figure from Q1.

Trends among new customers

- Lump sum lifetime mortgagesmade up a 45% share of new plans arranged in Q2 2020, compared to a 43% share in Q1 2020.

- Among the 3,328 new lump sum lifetime mortgages taken out (down 31% from the previous quarter), the average loan size dipped below £100,000 for the first time since Q3 2019 to to £99,959

- Drawdown lifetime mortgagesremained the most popular type of new plan agreed, albeit with a lower share (55%) of new customer activity than the previous quarter (57%).

- Amongthe 4,011 new drawdown plans taken out (down 36% from the previous quarter), the average first instalment (£68,606) was virtually unchanged from Q1 (£68,492). The average amount reserved for future use (£37,500) was 4% lower than in Q1.

Trends among returning customers

- Q2 2020 saw 5,608 customers returning to take extra drawdowns from their agreed reserves, compared to 9,805 in the previous quarter, as people exercised caution before making use of the option to access further funds. This is a 43% decrease from Q1 to Q2, compared with the 34% decrease in new customers served.

- The average drawdown instalment taken was £13,005 in Q2, compared with £11,611 in Q1.

- Further advance activity was also considerably quieter, with just 668 existing customers agreeing additional funds – the lowest number since Q1 2017.

Data tables:

Table 1: Average amounts of property wealth accessed by equity release customers, Q2 2020

| Quarter | Lump sum lifetime mortgages | Drawdown lifetime mortgages | Home reversion plans | ||||

| Average new plan | Average further advance | Average new plan – first instalment | Average drawdown amount taken | Average further advance – first instalment | Average new plan | Average further advance | |

| Q2 2020 | £99,959 | £24,395 | £68,606 | £37,500 | £13,809 | £36,784 | £31,580 |

| Q1 2020 | £102,443 | £22,738 | £68,492 | £39,214 | £12,250 | £46,235 | £25,005 |

| Q2 2019 | £93,712 | £21,586 | £63,166 | £35,903 | £11,762 | £51,250 | £22,758 |

| Quarterly change | -2% | 7% | 0% | -4% | 13% | -20% | 26% |

| Annual change | 7% | 13% | 9% | 4% | 17% | -28% | 39% |

Source: Equity Release Council, Q2 2020 market statistics

Please note: Due to being a smaller segment of the market and number of plans involved, fluctuations in home reversion plans figures are common.

About the data:

The Equity Release Council’s market statistics are compiled from member activity, including all national providers in the equity release market. This latest edition was produced in July 2020 using data from customer activity during the second quarter of this year (April to June). All figures quoted are aggregated for the whole market and do not represent the business of individual member firms.

Equity release products are available to homeowners aged 55+, enabling them to release money from the value of their home following a regulated process of financial advice and independent legal advice to determine whether this is suitable for their individual circumstances and long-term needs. Funds released are typically used for a range of purposes including providing additional retirement income, funding one-off expenses and lifestyle purchases, consolidating debts, meeting homecare costs and gifting a ‘living inheritance’ to family or friends.

For a comprehensive list of members, please visit the Council’s online member directory.

*Bank of England Money and Credit Series data, comparing February-March to April-May 2020.

Kindly shared by Equity Release Council

Main article photo courtesy of Pixabay

{kind=link}