Equity Release Council publish their Q3 2021 equity release market statistics

Equity Release Council publish their Q3 2021 equity release market statistics, showing homeowners set to access more than £4bn of property wealth this year via equity release for the first time on record.

Headlines from statistics:

- Over-55 homeowners unlocked £1.15bn of property wealth via equity release during Q3 2021, down 2% from Q2 (£1.17bn) but up 19% (£963m) compared with Q3 2020 as the UK was emerging from the first wave of the pandemic

- New and returning customers have accessed £3.46bn so far in 2021 – surpassing previous years and putting the market on track for over £4bn of activity this year

- Fewer customers access drawdown funds in Q3, but new plans and further advances both saw growth

- Average new lump sum plans reduced from £129,558 in Q2 to £121,464 in Q3 as the first Stamp Duty holiday deadline passes, while the average new drawdown plan size is unchanged.

David Burrowes, Chairman of the Equity Release Council, said:

“The equity release market has been a steady ship in turbulent times with activity broadly stable now for four successive quarters. The inevitable pandemic slowdown has been followed by the gradual return of confidence, helped by the robust performance of the wider property market.

“While annual activity has hovered close to £4bn since 2018, the market hasn’t stood still, and the available product range has more than doubled since then. Homeowners in need of extra funds for later life are increasingly look to equity release as a positive step, in the right circumstances, to benefit from a source of wealth they have built up over many decades.

“The Stamp Duty holiday inevitably impacted consumer behaviour over the summer and into autumn, with average loan sizes and drawdown activity fluctuating. Looking ahead, the ability to gift money to family members and share the proceeds of long-term house price growth is likely to remain an attractive option. Equity release can both help to close the financial gap between generations and allow people in later life to experience and enjoy the benefits of providing a living inheritance.”

Key statistics for Q3 2021 – Overall activity:

- Over-55 homeowners accessed £1.15bn of property wealth in Q3 2021. This was down 2% from £1.17bn in Q2 2021 but up 19% year-on-year from £963m in Q3 2020 when pandemic restrictions were tighter.

- The latest figures mean lending to new and existing customers has now exceeded £1bn for four successive quarters for the first time on record. This has been helped by a backlog of demand from successive lockdowns, the strong performance of the property market and further improvements in equity release product availability.

- A total of 19,300 new and returning customers were served between July and September as the market moves back towards pre-pandemic volumes of business. [see graph 1]

Key statistics for Q3 2021 – Trends among new customers:

- Customers agreed 10,023 new equity release plans in Q3 2021, up from 9,898 in the previous quarter, although this was 3% lower than a year earlier when activity in Q3 2020 was driven up by a backlog from the first Covid-19 lockdown.

- Drawdown lifetime mortgages remained the most popular product category, attracting 57% of new customers in Q3 2021 compared with 55% in Q2, while 47% chose a lump sum lifetime mortgage.

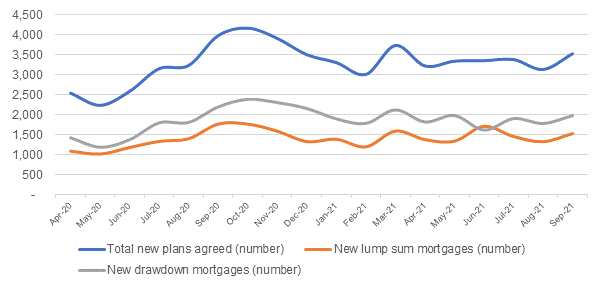

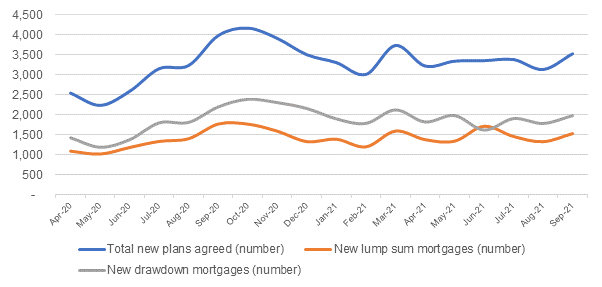

- September was the second busiest month of the year to date for new plans agreed (3,520), compared with 3,727 in March 2021 ahead of the original £500,000 Stamp Duty holiday deadline. August was the second quietest month of the year so far with 3,127 new plans agreed (compared with 3,003 in February). [see graph 2]

- The average first instalment of a new drawdown lifetime mortgage was £86,337, almost identical with Q2 (£86,349), with an additional £34,406 held in reserve (vs. £34,310 in Q2).

- The average new lump sum lifetime mortgage reduced by 6% from Q2 to £121,464 as the Stamp Duty holiday threshold dropped from £500,000 to £250,000 after 30 June. Larger loans during Q2 were likely to be influenced by customers’ desire to gift money to support family members’ house purchases or use equity release to make their own purchase before the deadline arrived.

- This latest average lump sum plan remains higher than any quarter prior to 2021 but is the lowest average so far this year. The long-term rise is likely to be influenced by rising property prices and more affluent customers using equity release products. The Council’s research shows the average house price among new lump sum customers was 17% higher in H1 this year than H1 2020.

Key statistics for Q3 2021 – Trends among returning customers:

- Q3 2021 saw 8,002 existing customers with drawdown lifetime mortgages return to make a withdrawal from their agreed reserves. This was the second highest figure since the pandemic broke out, although down from 9,382 during Q2 when the Stamp Duty deadline may have incentivised gifting from drawdown reserves to support house purchases.

- Further advances were agreed for 1,275 existing plans between July and September 2021, as customers sought to unlock additional property wealth. This was the highest level recorded in any quarter and was likely influenced by people looking to capitalise on the increase in property prices over the last 12 months, which has exceeded the average interest rate on equity release products in most regions of the country³.

Market data:

Graph 1: Equity release customers numbers, by type of customer, Q1 2017 to Q3 2021

Source: Equity Release Council

Graph 2: New equity release plans agreed per month, April 2020 to September 2021

Source: Equity Release Council

The Equity Release Council’s market statistics are compiled from member activity, including all national providers in the equity release market. This latest edition was produced in October 2021 using data from customer activity during the second quarter of the year (July – September). All figures quoted are aggregated for the whole market and do not represent the business of individual member firms.

Kindly shared by Equity Release Council (ERC)

Main photo courtesy of Pixabay

{kind=link}