Number of UK mortgage applications fell sharply in the final quarter of 2022

UK Finance today (9 March) releases its latest Household Finance Review in collaboration with Accenture, which shows a decline in consumer confidence and a drop in mortgage applications in Q4 2022.

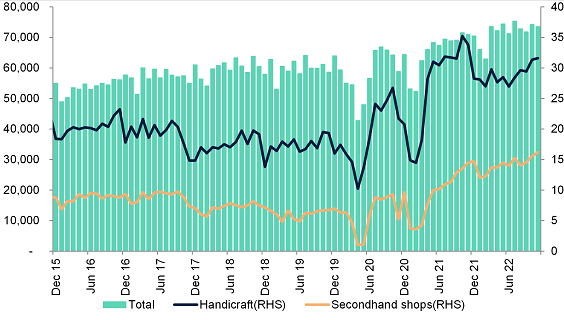

At the same time, concerns around the environment and the rising cost of living prompted a shift in spending away from luxuries, towards second-hand and DIY shopping.

Confidence and spending

Following the September 2022 mini-budget, consumer confidence fell below already-low levels. Despite the concerns of households about their finances, overall card spending remained steady in Q4. However, the data shows that there were clear changes in the way consumers were spending their money.

Spending on travel, particularly air travel, which had seen significant growth in the early months of 2022, fell away sharply in the final quarter of 2022. Other areas saw a marked increase in spending such as second-hand shops, handcraft stores and DIY stores, which all saw a sharp and sustained rise throughout 2022. While this can be seen as a symptom of the rising cost of living, these changes in consumer spending patterns also reflect a societal shift towards recycling and upcycling.

Meanwhile, personal loan borrowing – which is often used to fund more expensive purchases – saw a decline of nine per cent at the end of last year compared to the same quarter in 2021. Household savings remained essentially flat in Q4. However, following nearly a decade of decline in longer-term savings, there was growth at the end of last year as increasing savings rates boosted demand.

Chart 1 – Card spending in month, £mn

Mortgage market

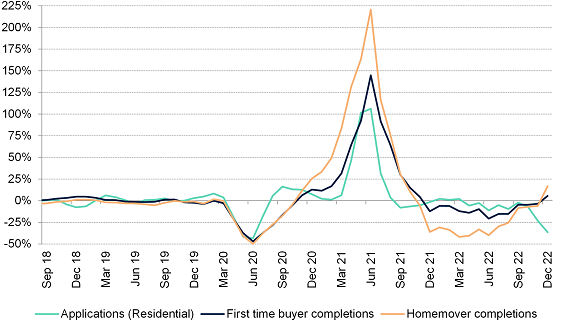

Overall, gross lending in the mortgage market grew by 1.9 per cent last year. House purchase activity was weaker throughout 2022 compared with a bumper year in 2021, but this was offset by rising house prices and a strong refinancing market.

Following the September mini budget the flow of mortgage applications submitted to lenders fell sharply to levels considerably below those seen in the final quarter of 2021.

At the same time, affordability constraints meant that a greater number of households are borrowing over a longer mortgage term, with the average term for a first-time buyer loans now at around 31 years.

Chart 2 – Mortgage applications and completions, three-month moving average, year-on-year change

Interest rate rises and cost of living pressures contributed to a modest rise in the number of people in arrears in Q4. The range and extent of mortgage forbearance available from lenders has helped keep arrears down, and we would encourage anyone struggling with their payments to speak to their lender as early as possible to talk through the options available to help.

Meanwhile, there were a little under 4,000 possessions over the whole of 2022. Whilst slightly up from the previous two years due to the industry’s voluntary pause on possessions, this is still lower than any other year since 1980 when the overall stock of mortgages was a little over half the size it is today.

Eric Leenders, Managing Director of Personal Finance at UK Finance, said:

“Despite the fall in applications towards the end of 2022 the mortgage market remains steady.

“Looking ahead, we expect a softer market compared with the past two years as cost pressures weigh on households, although refinancing levels will be robust due to the 1.8 million fixed rate deals scheduled to end this year.

“At the same time, consumers are changing the way they spend their money, moving away from luxury spending to second-hand shopping.

“As cost of living pressures persist throughout this year, many people may need to draw upon their savings to help with their bills.

“Lenders are looking to help anyone who is worried about their mortgage, loan or credit card payments.

“Those worried about their finances should speak to their lender as soon as possible to discuss the options available.”

Krishnapriya Banerjee, a managing director in Accenture’s UK banking industry group, said:

“A healthy mortgage market has historically been crucial to a healthy banking market, and the significant drop in mortgage applications late last year will have lenders keeping a watchful eye on the sector moving forward.

“With affordability stretched by a combination of higher rates and house prices, a growing number of households are seeking longer mortgage terms – with the average term for a first-time buyer loan now around 31 years.

“To help households, banks can provide the right mix of financial support and digital services to boost financial literacy.”

Kindly shared by UK Finance

Main article photo courtesy of Pixabay

{kind=link}