Mortgage market forecast to be weaker amid affordability pressures

This week UK Finance published its housing and mortgage market forecast for 2023 and 2024, showing it to be weaker amid affordability pressures.

In the face of the ongoing cost-of-living squeeze and rising interest rates, we expect a softer market for house purchases.

As we move into what the consensus forecast expects to be a period of protracted – if relatively shallow – recession, the situation is very different to that seen during the global financial crisis which saw investors withdraw from wholesale mortgage funding.

Now, funding lines remain intact, and lenders are ready to provide mortgages to customers. However, the barriers are likely to be on the demand side. Prospective borrower incomes need to be sufficient to cover both their mortgage payments and normal household expenditure, and both have risen considerably over and above the rate of wage growth this year.

With these pressures expected to persist over the forecast horizon, the picture is likely to be one of constrained effective demand for the purchase market through that period. We are already seeing a marked shift towards higher income households being the ones able to borrow for house purchases and this is likely to continue, leaving a smaller pool of potential borrowers until real wages adjust.

Chart 1: Residential mortgage lending, £ billions

Source: UK Finance

Refinancing will be strong, but may shift towards internal business

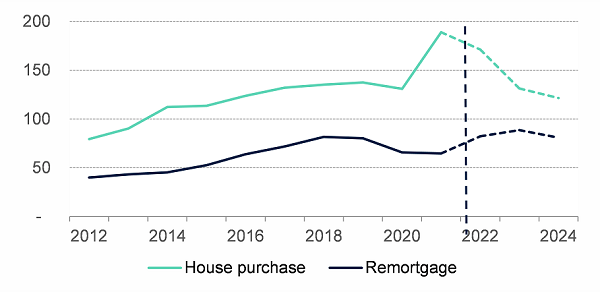

The other element of gross lending – remortgaging – is set for another strong year, having been the key driver of lending growth in 2022. With around 1.8 million fixed rate mortgages set to reach the end of their deal rate in 2023, these customers will be looking for a new deal.

However, as we set out in our Q3 Household Finance Review, escalating cost-of-living pressures coupled with materially higher interest rates than when households took out their current mortgage mean many customers, particularly amongst lower-income households, will have materially less “wiggle room” left over in their household budgets after refinancing. This affordability challenge means these customers may find their remortgaging options more limited on the open market.

The widespread availability of internal Product Transfers (PTs), which are not subject to the same stringent affordability tests, will mean the majority of customers will be able to find a new deal. However, this does bring a level of uncertainty to our forecasts, with respect to the mix within refinancing business between external remortgaging. This refinancing forms part of gross mortgage lending as published by the Bank of England, and Product Transfer business, which is not contained within gross lending figures. Should there be a further shift towards PTs because of these affordability constraints, this will bear down on reported remortgaging and, therefore, on overall gross lending next year.

Rising costs and payments to weigh on ongoing affordability, but upwards pressure on arrears expected to be relatively modest

Affordability pressures, both from rising inflation and interest rates, will inevitably put pressure on overall household finances next year and, within this, on mortgage payments.

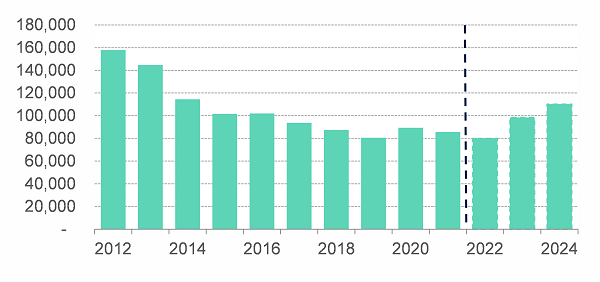

However, with a relatively modest increase in unemployment predicted through the forecast period, we expect the vast majority of borrowers to still be able to keep up with their mortgage payments. The number of customers in arrears is forecast to rise from the 80,000 seen at the end of September 2022 to a little under 100,000 by the end of 2023 (Chart 2).

Chart 2: 1st charge mortgages in arrears1

Source: UK Finance

Notes: 1. Arrears measured as those representing more than 2.5 per cent of outstanding mortgage balance

Although this would represent around a 23 per cent increase, this needs to be taken in context – the current figure is near to its historic low and the anticipated increase would still see numbers some seven per cent below the average over the past decade, and over 20 per cent below the average seen since 2000.

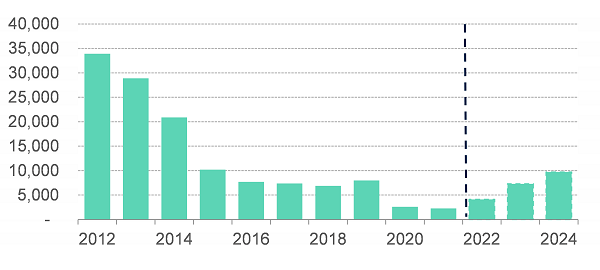

Meanwhile, we expect mortgage possessions to also rise modestly through the forecast period, totalling 7,300 next year and 9,800 in 2024 (Chart 3).

Chart 3: 1st charge mortgage possessions

Source: UK Finance

As with arrears, these are significant percentage increases from an abnormally low base. Numbers would remain low by any historic comparison, excluding the past three years of suppressed activity. Throughout the forecast horizon, most possession cases will arise from historic arrears either predating or exacerbated by the pandemic. We do not expect any “new” possessions activity, arising from affordability or other new pressures on household finances, to emerge until the end of 2024.

As always, we strongly urge customers worried about paying their mortgage to speak with their lender at the earliest opportunity. The industry stands ready to help with a range of forbearance options which can be tailored to best suit individual customers’ circumstances and help them navigate this challenging period.

Kindly shared by UK Finance

Main article photo courtesy of Pixabay

{kind=link}