The Equity Release Council publishes their Autumn 2021 Market Report

The Equity Release Council publishes their Autumn 2021 Market Report, which shows mortgage repayments soared 20% to reach a record £38bn in H1 2021.

Headlines:

- UK mortgage capital repayments have increased by 20% year-on-year, bringing the total amount of debt repaid in the first half of 2021 to an unprecedented £38bn – equivalent to £200m a day or £3,500 for every mortgaged household.

- The trend has been fuelled by regular repayments and overpayments reaching record hights, new borrowing ahead of the Stamp Duty deadline and fewer mortgage payment holidays.

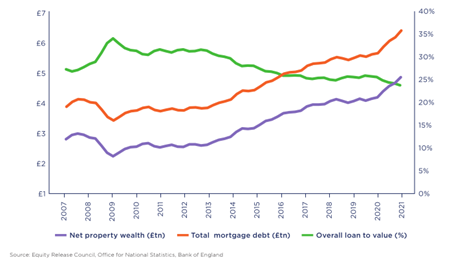

- Nation is now carrying over £1.5trn of mortgage debt for the first time on record, but factors including house price rises mean for every £1 of mortgage debt, there is more than £3 of equity in our homes.

- The overall value of UK housing stock has risen from £5.67trn to £6.42trn over the last year, with private property wealth reaching a new high of £4.87trn.

- Lifetime mortgage product options have doubled in the last two years which, combined with low rates and flexible features, increases the appeal of using equity release to help meet later life financial needs.

David Burrowes, Chairman of the Equity Release Council, comments:

“UK households are converting unprecedented amounts of mortgage borrowing into property wealth as we look to move on from the worst of the pandemic. Combined with property price rises fuelled by the Stamp Duty holiday, homeowners have record equity to potentially draw upon in later life.

“The transformation of later life mortgages in recent years has given people more opportunities to access their biggest source of wealth. We are seeing mindsets change to the point that tapping into property wealth is now a common consideration to meet various retirement needs, from topping up pension income to providing a ‘living inheritance’ via gifting to younger generations.”

“The modern equity release market has shown resilience in the face of uncertainty to climb back towards pre-pandemic levels. The disruption of the last 18 months has not slowed the pace of innovation in lifetime lending, and it is important the market continues to evolve to address the financial challenges people will face in the post-pandemic world.”

Key statistics – Market context:

- Strong performance in the housing market saw UK private property wealth increase from £4.21 trillion at the end of H1 2020 to an unprecedented £4.87tn at the end of H1 2021.

- The overall value of UK housing stock rose from £5.67tn to £6.42tn over the last year.

- Households repaid more than £19bn of mortgage capital during both Q1 and Q2 2021, having never repaid more than £18bn in any previous quarter.

- Rising property prices means more than three quarters of the value of the average home is tied up in equity rather than debt, leaving £201,642 of property wealth for its owner to draw on.

- House price rises over the last year will have helped to balance out the impact of compound interest for some existing equity release customers. With the annual rate of UK house price growth having been above 7% since January 2021, a customer paying 6% interest could have seen their property equity grow faster than their loan, while a customer paying 3% interest could have seen their equity grow more than twice as fast.

Key statistics – Overall customer activity:

- Across the first half of 2021,35,860 new and returning customers were served, unlocking £2.3bn of property wealth to support their finances.

- Customer numbers steadily rose in H1 2021 with June seeing the most new plans agreed (3,348).

- New customer levels remained broadly consistent with those seen in H2 2020, dipping slightly from 21,917 to 21,596 new plans taken out, but higher than this time last year when the first lockdown slowed activity (18,420 new plans).

- Returning drawdown numbers remained subdued – a trend that has persisted since the onset of the pandemic – while the number of further advances agreed was slightly below that of H2 2020.

Key statistics – Product features and pricing:

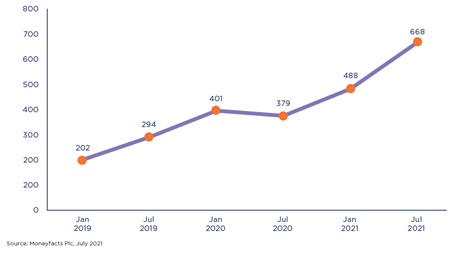

- The total number of equity release products available increased to a record high of 668 in July 2021, from 448 six months earlier. Customers have access to more than double the number of product options than two years ago.

- Strong competition has meant consumers have access to double (127%) the number of product options than two years ago.

- More than two thirds (68%) of products allow customers to make voluntary capital repayments with no early repayment charge, while nine in 10 (89%) products offer fixed early repayment charges.

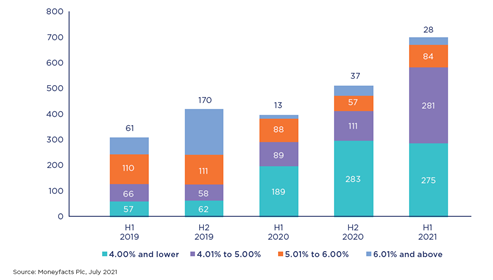

- The average equity release rate crept up modestly to 4.26% but there are still more options available today with rates of 4% or lower than a year ago.

- Interest rates have plummeted by nearly two percentage points over the last five years.

Key statistics – Customer trends:

- The average age of new customers remained stable in H1 2021 at 70 years old for new drawdown customers 68.4 for new lump sum customers.

- Almost a third (30%) of new drawdown single plans are being taken out by female customers, the highest level seen in the last two years.

- The average house price of new customers continues to rise to record levels for both new drawdown (£419,166) and lump sum (£406,139) plans. This comes as UK property prices have increased over the last year to reach an average of £265,668

- Across new lump sum and drawdown customers, the average amounts of property wealth released increased slightly but were offset by higher house prices, meaning loan-to-values remained stable.

Graphs:

UK trends in private property wealth

Number of equity release products at different price bands

Number of products available in the equity release market

Equity release product features

| 53% of products are available to customers living in sheltered or age-restricted accommodation, subject to individual lender requirements | 39% of products allow customers to make regular full or partial interest payments |

| 68% of products allow voluntary capital repayments with no early repayment charge | 50% of products enable downsizing repayment options, so the loan can be repaid with no early repayment charge if the customer opts to downsize in future |

| 89% of products offer fixed early repayment charges | 55% of products offer drawdown facilities |

| 26% of products offer an inheritance guarantee, to ringfence part of the property’s value as a minimum protected amount to leave behind | 2% of products allow customers to receive regular income payments |

Source: Product data supplied by Key, July 2021

Kindly shared by The Equity Release Council (ERC)

Main photo courtesy of Pixabay

{kind=link}